Shoppers, especially those on GLP-1 medications, say they want to eat more fruits and vegetables, but data shows produce has to work harder to turn that intention into real growth.

As retailers and suppliers look toward the rest of 2026, the message from a recent webinar hosted by the International Fresh Produce Association and Circana was clear: Consumers are still buying produce, but the “why” behind those purchases is shifting in meaningful ways.

Performance Holds Steady in a Tighter Food Economy

Jonna Parker, principal of Circana, opened the webinar with a reminder that food retail overall remains resilient; amid weather disruptions and ongoing affordability pressures, total food and beverage sales have held up. Produce, she notes, “is still holding strong with its place as an important, vital part of total U.S. edible sales.”

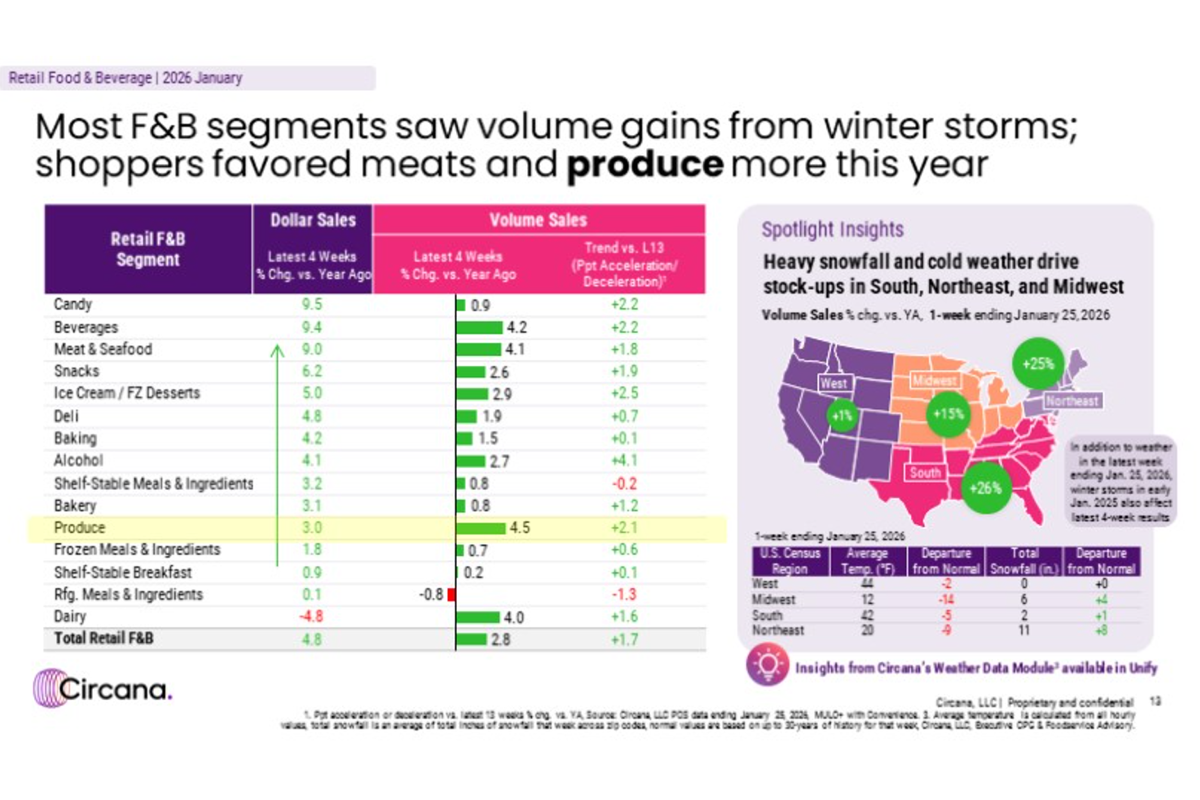

Over the latest 52 weeks, retail produce dollar sales grew 2.3%, slightly below total food and beverage growth of 2.9%. Volume, however, tells a stronger story. Produce pounds sold increased 1.9%.

“Produce had the most pound increase or volume increase of any other department,” Parker says, calling it one of the first times in recent years she could make that claim.

At the same time, pricing has moderated. Average price per volume in produce rose just 0.5%, far below many center-store categories. Parker describes value as one of produce's superpowers, especially compared to ultra-processed foods and protein products that have seen steeper price inflation.

Yet headwinds remain. Traditional supermarkets continue to lose share to mass, club and e-commerce channels. Online sales account for only 9% of produce dollars, but they drove 60% of incremental dollar growth in the category last year. Parker says consumers “don't want friction. They want what they want, when they want it.”

Fewer Calories, More Intention

One of the most significant macro shifts affecting produce is a decline in overall calorie consumption. For the first time in decades of tracking, Circana saw a drop in per capita calorie intake in 2025.

“When there's less per capita calories, it means it's a bigger fight than ever to get folks to buy what we want them to buy as food marketers,” Parker says.

Consumers are not just eating less; they are eating more intentionally. Health, affordability and lifestyle fit are being weighed together in each decision.

“This year of affordability has made every decision by a consumer be … in context,” she says.

Shoppers are thinking about trade-offs across the basket, not just within categories. That intentionality is especially visible in the rise of GLP-1 medications.

GLP-1 Users: Aspiration vs. Reality in Produce

Circana's latest research shows that 15% of U.S. households now have at least one member taking a GLP-1 medication. Weight loss is the primary driver, up 41 percentage points since 2021, as the stated reason for use. Most users are on the medication for six to 12 months, though shorter-term use may increase as access expands and prices fall.

The top-line insight for produce is nuanced.

“Ultimately, when recently on the drug, they do seek more fruits and more vegetables, right along with more protein,” Parker says. “Literally, they aspire to eat more. The majority of people on the drugs aspire to eat more fruits and veggies, and they expect to eat less of sugar, carbohydrates and sodium.”

But aspiration has not yet translated into stronger produce performance.

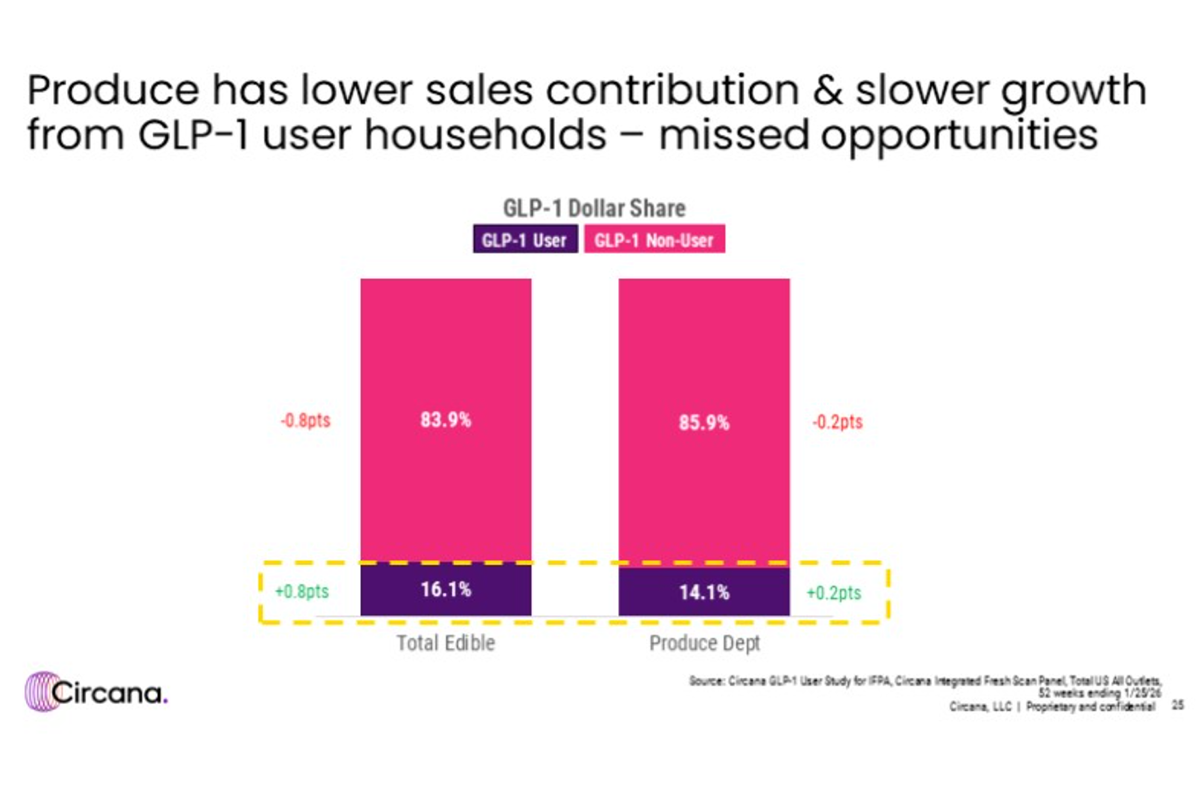

GLP-1 households account for 16% of total food and beverage dollar sales, yet only 14% of produce dollars. Despite growth in usage, produce has not gained incremental share from these shoppers.

“In almost every major category, the quantity of units in that category being bought by GLP-1 households is less than the quantity bought by non-users,” Parker says. “By no means are we seeing people suddenly buy more of any of these fruits and vegetables than those who are not on GLP-1 drugs.”

That gap between intent and purchase represents an opportunity. Center-store brands are leaning into explicit GLP-1-friendly messaging, protein callouts and functional claims. Produce, by contrast, has largely relied on assumed health halos.

“If you think that the health romance that's happening right now in America is naturally going to drive fruit and veg, it ain't happening,” Parker says.

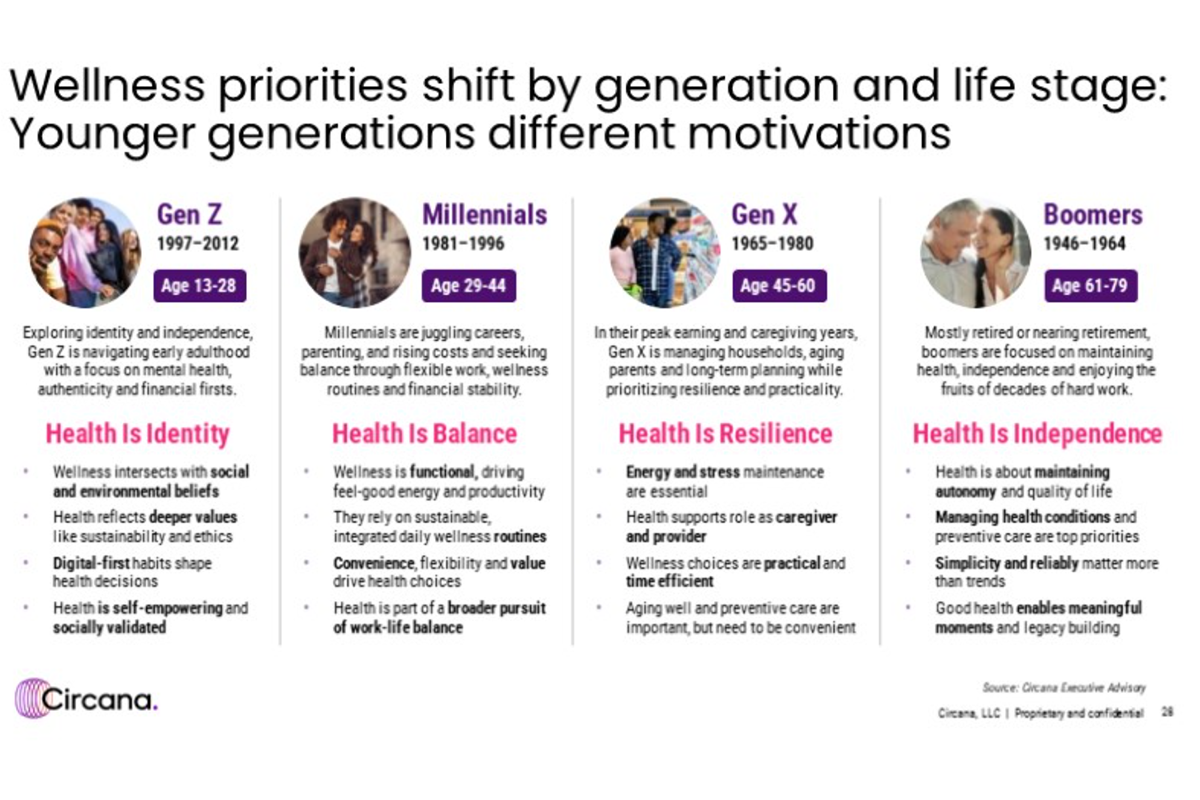

Generational View: Same Health Goal, Different Motivations

Health may be universal, but how it resonates differs sharply by generation.

Across markets, IFPA's global research shows health is consistently a top-three purchase driver for produce. In Brazil, 85% of consumers cite health as a motivator; in China, 75%; and in the U.S. and Germany, 64%.

Yet health alone rarely closes the sale. In the U.S., affordability leads at 76%. In Germany and South Korea, trustworthiness tops the list. In the United Kingdom, quality leads.

Rachel Blake, manager of global insights for IFPA, summarizes the conversion formula: “You need to lead your messaging with health. It gets attention, but close with whatever your market's conversion lever is: trust, quality or value.”

Generationally, the contrast is just as pronounced.

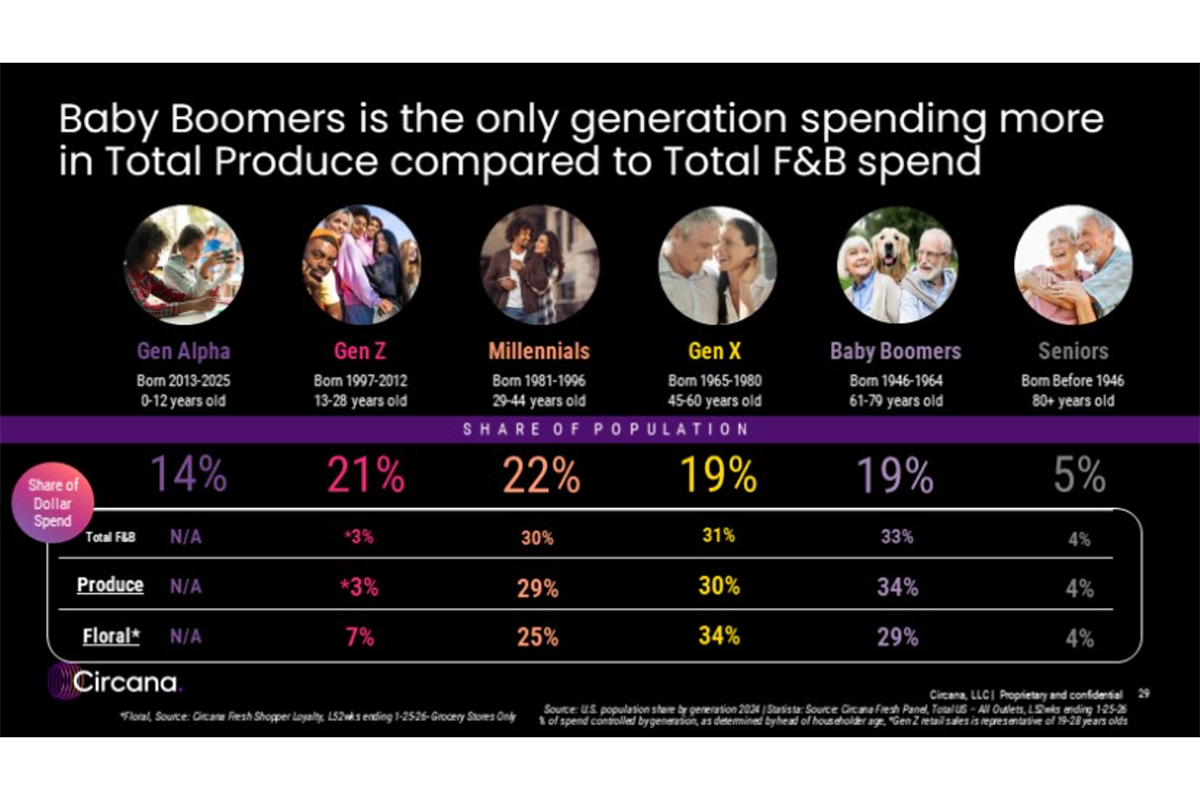

Baby boomers remain the backbone of produce spending and are already committed to healthy eating. In the U.S., 52% of baby boomers report concern about daily healthy eating. In Germany, 75% consume fresh fruit regularly. They respond to fundamentals such as nutrients and longevity.

Gen Z and millennials, however, approach health through a lifestyle lens. Their goals center on functionality, feeling better and looking better. Social media is their primary source of inspiration. Nearly half of Gen Z, millennials and Gen X consumers cite social platforms as dominant sources for everyday cooking ideas.

“They won't just naturally find us,” Parker says.

Younger shoppers spend less time in store and more time discovering foods online. Trend exposure in beverages or snacks often precedes fresh purchases. Mango, for example, has benefited from earlier adoption in drinks and dried fruit before accelerating in fresh.

When asked what would motivate them to try more fruits and vegetables, younger consumers overindexed on seeing new flavors, pairing ideas and recommendations from trusted advisers or influencers.

The assumption that younger generations will eventually shop like Gen X and baby boomers is misguided.

“If you're waiting for that moment … it's not coming,” Parker says.

The Mandate: Be Intentional, Because Consumers Are

Consumers have adapted to inflation, to omnichannel shopping and now to appetite-suppressing medications. They are more intentional about how they spend calories and dollars.

Produce remains uniquely positioned as the department people aspire to eat more of, yet aspiration alone is not enough.

The data suggests three imperatives:

- Reinforce value clearly and consistently.

- Translate health into functional, lifestyle-relevant messaging, especially for younger shoppers.

- Speak directly to emerging segments such as GLP-1 users rather than assuming the halo will carry the category.

As Parker puts it, success hinges on “understanding what truly drives choice across the infinite number of options that consumers have.”

In a lower-calorie, higher-intent food economy, produce still has the credentials. The challenge is making sure those credentials are visible, relevant and actionable for every generation.