Editor’s note: This column is part of an ongoing series, The 30 Different Plants Per Week Challenge, Retail Edition.

For nearly a century, the American grocery store was built on a stable foundation of the center store, packed with refined grains, cereals and shelf-stable goods, which was the high-margin engine that subsidized the “risky” perishables on the edges.

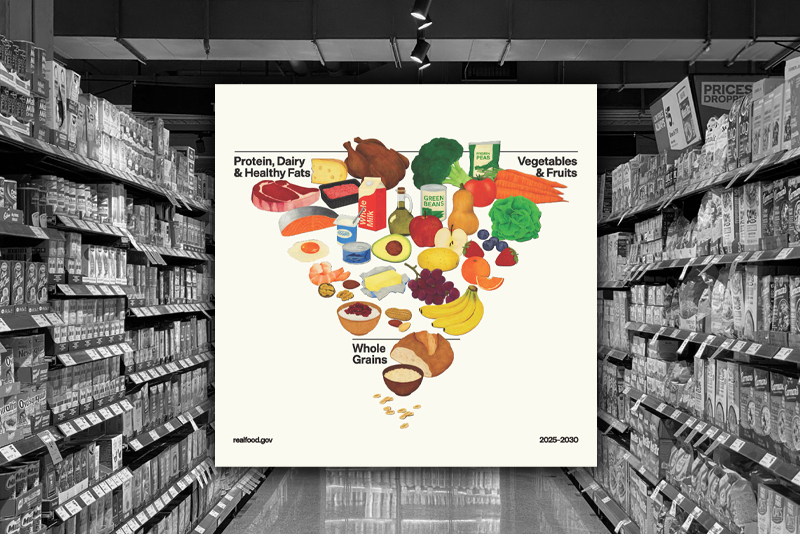

But as of 2026, the federal government has shaken up the food pyramid. By placing fresh produce and whole proteins at the base and relegating processed grains to the “use sparingly” tip at the bottom of the inverted pyramid, it has potentially changed how Americans eat, along with the traditional retail economic model.

It is an economic earthquake with a $130 billion epicenter. According to the March 2026 Numerator “Food Pyramid Flip” report, the federal transition from a grain-based foundation to a produce-and-protein-heavy base carries a price tag of $1,012 per household per year. For a retail industry built on the thin margins of shelf-stable goods, this 32% increase in per-person monthly spending represents the largest reallocation of consumer capital in the modern era.

While the new pyramid mandates a diet where fresh produce and whole proteins occupy the largest share of the plate, middle-income households — the traditional engine of grocery volume — currently maintain the lowest share of perimeter spending. This creates a massive disconnect between federal policy and household liquidity.

Currently, the center store (packaged and refined goods) still commands 49% of total grocery sales, while the fresh perimeter sits at 42%. However, the report indicates that low-trust consumers — those least likely to follow government mandates — are actually leading the migration, already allocating 48% of their dollars to fresh categories.

Logistics of an Inverted Inventory

The old food pyramid allowed for a retail model predicated on slow logistics. Refined grains and ultraprocessed snacks provided a buffer of shelf stability that subsidized the volatility of the produce department. The new food pyramid removes that buffer.

- Velocity shift: As fresh produce moves from a 12% basket share to a projected 28%, the inventory turn rate for the entire store must accelerate. The “Food Pyramid Flip” report highlights that whole-form vegetables and fruits are now the primary utility of the shopping trip, requiring a total recalibration of the cold chain to handle 2.5 times the previous volume.

- “Real food” premium: The $1,012 annual cost increase identified by Numerator isn’t evenly distributed. The report finds that for the bottom 40% of earners, the cost of adhering to the new pyramid consumes an additional 4.5% of their total disposable income, making “freshness at scale” the most significant hurdle for retail expansion in 2026.

Retailer Insights: Mapping the Displaced Dollar

The Numerator findings suggest that the death of the center store is being driven by a combination of regulatory pressure and shifting consumer trust profiles.

- Square footage reallocation: With 250,000 Supplemental Nutrition Assistance Program-authorized retailers now facing new mandates to double their stocking of healthy staples, the physical footprint of the store is changing. Retailers are moving away from the 50/50 split between dry and refrigerated space, with new store formats favoring a 65/35 perimeter-to-center ratio.

- Private-label pivot: The Numerator report found that 22% of shoppers cite a lack of clear on-package guidance as a primary barrier to following the new pyramid. This has opened a massive door for “clean-label” private brands. Instead of generic snacks, top-performing retailers are launching private-label produce kits — pre-washed, pre-cut and explicitly labeled to meet the new nutrient-density standards. This allows them to capture the convenience-seeking shopper who is fleeing the center aisles but remains wary of the high cost and prep time of the fresh perimeter.

- Trust factor: Interestingly, the 48% perimeter spend among low-trust households suggests that the move toward fresh produce is being viewed as a “self-reliance” or “clean-living” movement rather than a response to government nudging. This segment of the market is less responsive to traditional health claims and more focused on transparency and whole-form integrity.

Economic Reality of 2026

The “Food Pyramid Flip” has created a vacuum. As refined grains and sugars drop to less than 10% of the recommended basket, the $130 billion previously spent in those aisles is looking for a home. The Numerator data makes one thing clear: Money is flowing directly into the refrigerated racks. The challenge for the industry isn’t just stocking more spinach; it is managing the transition from a shelf-stable economy to a fresh-velocity economy where the produce department is the new anchor of the American grocery store.

Your Next Read: